How wars disrupt coal routes, scrap flows, freight rates, and steel pricing weeks before the news catches up

Not through headlines but through delayed vessels, rising freight quotes, inconsistent scrap quality, and sudden price corrections.

Steel is one of the earliest industries to react to geopolitical tension because it depends on globally interconnected raw material flows :

- Coal from Australia, Indonesia, South Africa

- Scrap from the US, Europe, Middle East

- Pig iron from Russia, Ukraine, Brazil

- Pellets from Brazil, Middle East, India

When conflict begins even before escalation, these flows start shifting.

And the impact shows up weeks before the world notices.

Why Steel Feels Conflict First

Steel sits at the intersection of :

- Energy

- Infrastructure

- Manufacturing

- Global trade

It consumes raw materials at massive scale :

- ~1.9 billion tonnes of steel produced globally per year

- 700+ million tonnes of seaborne coal trade annually

- 600+ million tonnes of scrap traded globally

This makes steel extremely sensitive to :

- Shipping disruptions

- Sanctions

- Fuel price volatility

- Currency movements

Even minor geopolitical signals can trigger major supply chain reactions.

1. Coal Routes Shift Before Supply Falls

Coal is the first to react, not because supply disappears, but because routes become uncertain.

What happens immediately :

- Shipping insurance premiums rise

- Vessel rerouting begins

- Charter rates increase

- Buyers rush to secure cargo

For example :

- Freight rates can jump 20–50% within days of geopolitical tension

- War-risk premiums can increase shipping cost by $3–$10 per tonne

Even if coal supply remains unchanged, land cost increases instantly.

Operational Impact on Plants

Higher freight leads to :

- sudden increase in fuel cost

- Pressure on furnace margins

- Procurement panic buying

In blast furnace operations :

- Coal cost contributes 30 – 40% of hot metal cost

A $10/tonne increase in coal landed cost can raise :

- Steel production cost by ₹800–₹1,200 per tonne

Plants feel this before any official supply shortage is reported.

2. Scrap Markets React Faster Than Any Other Raw Material

Scrap is the most volatile raw material during geopolitical uncertainty.

Why?

Because scrap is :

- Highly traded

- Easily redirectable

- Sensitive to export policies

Immediate effects of conflict :

- Export restrictions or slowdowns

- Hoarding by suppliers

- Reduced availability in key markets

Scrap prices can move :

- $30 – $80 per tonne within 2 – 3 weeks

In some past disruptions, price spikes of :

15–25% within a month

have been recorded.

Operational Impact in EAF Plants

EAF steelmaking relies on :

- 70 – 90% scrap in metallic charge

When scrap flow becomes uncertain :

- Plants shift to lower-quality scrap

- Chemistry variability increases

- Pig iron demand rises

This leads to :

- Higher power consumption

- More alloy correction

- Reduced yield

Even a 1% yield drop in a 500,000 tonne plant can cost :

- ₹20 – ₹25 crore annually

3. Pig Iron Becomes a Strategic Commodity Overnight

Pig iron is often overlooked until scrap becomes unreliable.

During conflict :

- Pig iron supply tightens

- Export flows from key regions are disrupted

- Prices rise sharply

Historical observations show :

- Pig iron prices can increase by 20 – 40% within weeks of supply disruption

Why Demand Spikes

When scrap becomes inconsistent :

- EAF plants increase pig iron usage to stabilise melt chemistry

- Foundries secure additional inventory

Pig iron shifts from :

supplementary material → critical stabiliser

This sudden demand surge tightens supply further.

4. Pellet Supply Tightens Through Indirect Effects

Pellets are less volatile than scrap but still affected.

Conflict impacts :

- Mining operations

- Port availability

- Shipping schedules

Even without direct supply cuts :

- Vessel delays increase

- Delivery timelines extend

Typical impact :

- Lead times increase by 7 – 20 days

- Prices rise by 5 – 15%

Operational Impact

Pellets are critical for :

- DRI plants

- Blast furnace burden stability

Delays force plants to :

- Increase reliance on lower-grade ore

- Adjust burden mix

- Increase fuel consumption

Even a 2% drop in reduction efficiency can increase fuel cost significantly.

5. Freight Becomes the Biggest Hidden Cost

One of the earliest and most underestimated impacts of conflict is freight escalation.

Shipping markets react instantly to :

- Route risks

- Port congestion

- Fuel price spikes

Typical freight changes during tension :

- Bulk shipping rates increase by 25 – 60%

- Container and bulk availability drops

For raw materials :

- Freight can account for 15 – 25% of landed cost

A $15 increase in freight can :

- Erase procurement savings

- Distort cost calculations

- Force renegotiation of contracts

6. Currency and Trade Flows Add Pressure

Geopolitical events often trigger :

- Currency volatility

- Trade restrictions

- Sanctions

For import-dependent countries :

- Currency depreciation increases landed cost

- LC (Letter of Credit) conditions tighten

- Payment cycles become longer

Even a 5% currency movement can significantly impact raw material cost.

7. Steel Prices Move Last, But Fastest

Interestingly, finished steel prices react after raw material markets.

Why?

Because :

- Producers try to absorb cost initially

- Inventory buffers delay price changes

- Contracts delay adjustments

But once raw material pressure builds :

- Steel prices adjust sharply

Typical pattern :

- Raw material prices rise first

- Steel prices follow after 2 – 4 weeks

- Market correction happens rapidly

Price increases of :

- ₹2,000 – ₹5,000 per tonne can occur within weeks

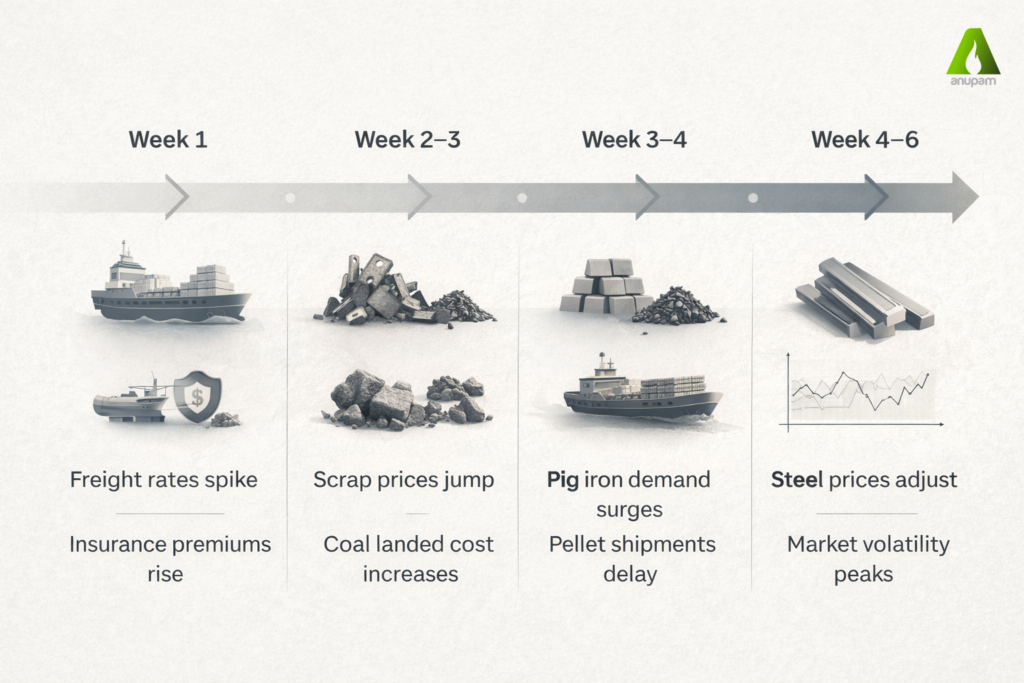

The Timeline of Impact

A typical conflict-driven disruption unfolds like this :

Week 1 :

- Freight rates spike

- Insurance premiums rise

Week 2 – 3 :

- Scrap prices jump

- Coal landed cost increases

Week 3 – 4 :

- Pig iron demand surges

- Pellet shipments delay

Week 4 – 6 :

- Steel prices adjust

- Market volatility peaks

By the time headlines focus on steel, the industry has already absorbed the shock.

Why the Impact Feels “Sudden”

To outsiders, price spikes look abrupt.

But inside the industry, they are the result of :

- early supply chain shifts

- procurement reactions

- inventory adjustments

Steel does not react late.

It reacts early but quietly.

How Smart Players Respond Early

Advanced steelmakers and suppliers monitor :

- Shipping patterns

- Freight indices

- Scrap booking trends

- Port congestion

- Currency movement

They act before disruption becomes visible.

Typical strategies include :

- Forward booking raw materials

- Diversifying sourcing

- Increasing inventory buffers

- Adjusting product pricing early

Early action reduces shock impact.

Steel Moves Before the News

Steel is not just an industrial product.

It is a real-time indicator of global disruption.

When :

- Freight rises

- Scrap tightens

- Coal costs shift

The industry already knows something is coming.

Long before headlines confirm it.