How gas shortages, oil price spikes, and policy changes ripple into coke demand, DRI production, and furnace economics?

Energy does not just power steel.

It defines how steel is made.

From coal – fired blast furnaces to gas-based DRI plants and electric arc furnaces, every steelmaking route is tied directly to energy availability, pricing, and policy.

So when energy politics shifts, whether through war, sanctions, OPEC decisions, or gas supply disruptions, the impact on steel is not gradual.

It is immediate.

And it begins long before steel prices move.

Steel Is an Energy Conversion Industry

At its core, steelmaking is the conversion of energy into metal.

Typical energy consumption :

- Blast Furnace route : 20 – 25 GJ per tonne of steel

- DRI + EAF route : 10 – 18 GJ per tonne

- EAF (scrap-based) : 350 – 450 kWh per tonne

Energy accounts for :

- 20 – 40% of total steel production cost

This makes steel one of the most energy-sensitive industries globally.

Even small shifts in energy pricing or availability ripple directly into :

- Raw material demand

- Process selection

- Furnace efficiency

- Profitability

1. Gas Shortages Disrupt DRI First

Gas-based Direct Reduced Iron (DRI) plants rely heavily on:

- Natural gas (CH₄)

- Reformer – based reduction processes

Typical gas consumption :

- 2.5 – 3.0 Gcal per tonne of DRI

When gas supply tightens :

- Prices spike rapidly

- Supply allocation becomes restricted

- Governments may prioritize power or domestic use

What Happens Inside the Industry

When gas prices rise :

- DRI production becomes uneconomical

- Plants reduce output or shut temporarily

- Supply of sponge iron tightens

Example impact :

If gas cost increases by 30 – 50% :

- DRI production cost rises by ₹2,000 – ₹4,000 per tonne

Chain Reaction

Reduced DRI output leads to :

- Increased demand for scrap

- Higher reliance on pig iron

- Pressure on blast furnace output

DRI is often a stabilizer in steelmaking.

When it disappears, the system becomes volatile.

2. Oil Price Spikes Increase Everything – Quietly

Oil does not directly produce steel.

But it controls :

- Shipping costs

- Mining operations

- Logistics

- Heavy equipment fuel

When crude oil rises :

- Freight rates increase

- Mining costs rise

- Transportation becomes expensive

Typical Impact of Oil Price Increase

A $10 increase in crude oil can :

- Raise freight rates by 10 – 20%

- Increase landed coal cost by $5 – $12 per tonne

For a plant importing 1 million tonnes of coal annually :

- That’s an additional ₹40 – ₹100 crore cost impact

Hidden Effect : Logistics Disruption

Higher fuel costs lead to :

- Slower shipping cycles

- Vessel shortages

- Port congestion

This delays raw material availability, affecting furnace continuity.

3. Coke Demand Rises When Gas Falls

When gas becomes expensive or unavailable :

- DRI production drops

- Blast furnace production increases

This shifts demand toward :

- Metallurgical coke

- Coking coal

Why Coke Becomes Critical

Blast furnaces depend on coke for :

- Structural support

- Reduction reactions

- Heat generation

Typical coke consumption :

- 300 – 450 kg per tonne of hot metal

When DRI falls out of the system :

- Coke demand rises sharply

- Coke prices increase

Observed Market Behavior

During energy disruptions :

- Coke prices can increase by 15 – 30% within weeks

- Coking coal demand spikes globally

Plants that rely heavily on coke face :

- Higher input costs

- Tighter supply conditions

4. Pellet Demand Becomes Unstable

Pellets play a key role in :

- DRI production

- Blast furnace burden

When gas supply is stable :

- Pellet demand is high (DRI-driven)

When gas supply drops :

- Pellet demand shifts toward blast furnaces

What Changes in Pellet Markets

- Demand becomes unpredictable

- Pricing fluctuates

- Supply chains become strained

Typical impact :

- Pellet premiums can fluctuate by $10 – $25 per tonne

Operational Impact

Plants may :

- Change burden mix

- Increase sinter usage

- Adjust reduction strategies

This affects :

- Furnace efficiency

- Fuel consumption

- Slag chemistry

5. Policy Decisions Amplify Everything

Energy politics is not just about supply.

It is about policy decisions.

Governments may :

- Restrict exports

- Cap domestic prices

- Prioritize power generation

- Impose environmental controls

Examples of Policy Impact

- Gas allocation shifts from industry to power

- Coal export bans tighten global supply

- Carbon taxes increase production costs

Even a single policy decision can :

- Distort global trade flows

- Create artificial shortages

- Increase price volatility

6. Furnace Economics Change Overnight

Energy shifts directly impact cost per tonne of steel.

Let’s look at a combined effect scenario :

If :

- Gas price rises by 40%

- Coal freight increases by $10/tonne

- Coke prices rise by 20%

Then :

- steel production cost can increase by ₹3,000 – ₹6,000 per tonne

This happens before steel prices adjust.

7. The Lag Effect: Steel Prices React Last

Raw materials react instantly.

Steel prices react with delay.

Why?

- Inventory buffers exist

- Contracts delay price revision

- Producers absorb initial cost

But once pressure builds :

Steel prices adjust rapidly

Typical lag : 2 – 4 weeks after energy shock

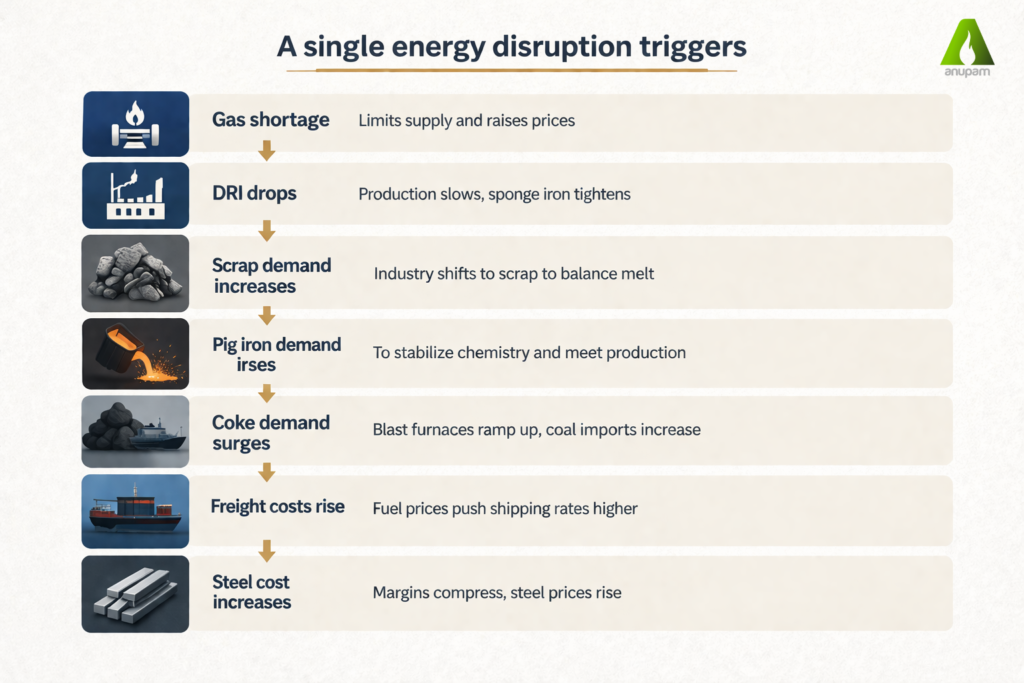

The Domino Effect of Energy Politics

A single energy disruption triggers :

Gas shortage

↓

DRI drops

↓

Scrap demand increases

↓

Pig iron demand rises

↓

Coke demand surges

↓

Coal imports increase

↓

Freight costs rise

↓

Steel cost increases

This chain reaction happens faster than market visibility.

Why Steel Feels It First

Steel sits at the intersection of :

- Energy

- Infrastructure

- Manufacturing

It consumes energy at scale and continuously.

Unlike other industries :

- Steel cannot pause easily

- Furnaces run continuously

- Supply chains must remain active

This makes it the first industry to absorb energy shocks.

What Smart Players Do Differently

Advanced steelmakers respond early :

- Diversify energy sources

- Hedge fuel costs

- Maintain flexible burden mix

- Secure long-term supply contracts

They treat energy as :

not just a cost – but a strategic variable

Energy Controls Steel Before Markets Do

Steel prices do not move first.

Energy does.

By the time steel prices react :

- Energy costs have already shifted

- Raw material markets have adjusted

- Margins have already been impacted